Get the Right Mortgage for you!

Cari McClelland. Mortgage professional.

I'm here to help you discover the perfect mortgage solution for your needs!

Cari McClelland

With over a decade of experience in human resources, Cari has developed a keen understanding of people and their needs. After a successful career dedicated to talent acquisition, employee relations, training and organizational development, Cari made the exciting transition to mortgage brokering.

Driven by a passion for helping others achieve their dreams of homeownership, Cari leverages their extensive background in HR to provide exceptional customer service and personalized financial solutions. Known for her strong communication skills and empathetic approach, she excels at guiding clients through the mortgage process with clarity and confidence.

Cari holds a certificate in Human Resources Leadership and is a licensed Sub Mortgage Broker. In her spare time, she enjoys exploring local neighborhoods, volunteering in community initiatives, and staying up to date with industry trends. Whether you’re a first-time buyer or looking to refinance, Cari is dedicated to making your mortgage experience seamless and rewarding.

Happy Clients

" Our heartfelt thanks for all you did over the past month to support our mortgage search. Your integrity and professionalism are evident Cari! We will pass your name with highest recommendation and gratitude. "

Finding the best mortgage can be frustrating. It doesn't have to be when you follow my 3 step plan.

Start your journey today

The best way to begin is by reaching out to me directly. I'm dedicated to understanding your needs, evaluating your financial situation, offering expert mortgage advice,

and

supporting you throughout the entire mortgage process.

Gain clarity

Navigating through various mortgage lenders, rates, terms, and features can be overwhelming.

Let me simplify things for you.

I’ll present the best mortgage options tailored to your needs, helping you make an informed decision.

Move forward with confidence

My goal is to ensure

you're always fully informed.

From your initial application to your mortgage renewal, I'm here to answer any questions and support you every step of the way. You can count on me to have your back.

Get started by completing my online mortgage application.

I'll let you know exactly where you stand so you can proceed with confidence.

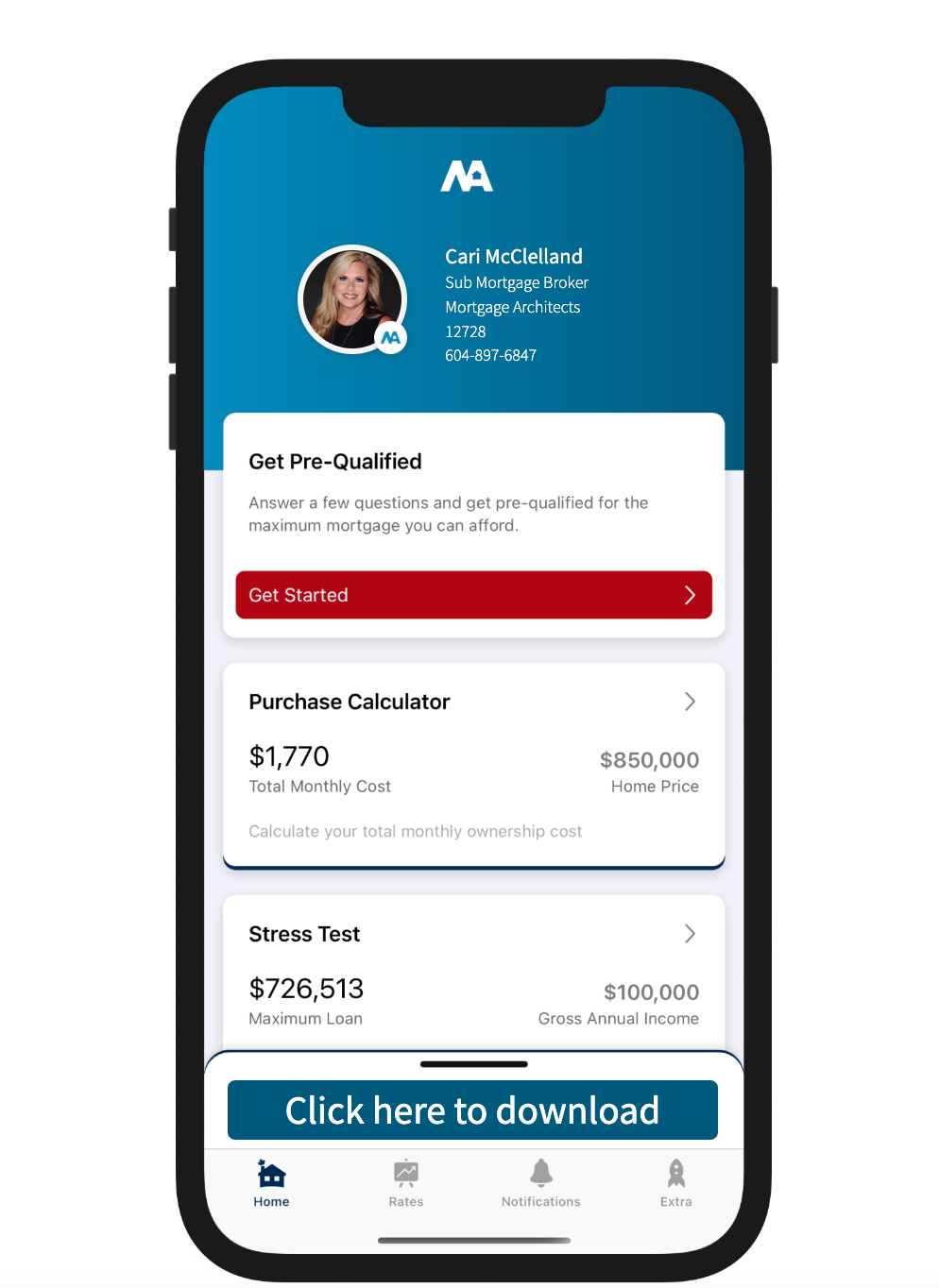

A mortgage app like no other!

What can you do with my app?

- Calculate your total cost of owning a home

- Estimate the minimum down payment you need

- Calculate Land transfer taxes and the available rebates

- Calculate the maximum loan you can borrow

- Stress test your mortgage

- Estimate your Closing costs

- Compare your options side by side

- Search for the best mortgage rates

- Email Summary reports (PDF)

- Use my app in English, French, Spanish, Hindi and Chinese

Everything you need, all in one place

As a trusted mortgage provider, let me help you with these services.

Let's Run Some Numbers

Mortgage articles to keep you informed.